College Savings

Turning Tax Refunds into College Savings

Families who save for college are generally better equipped to navigate financial aid, will not have their financial aid affected much by their savings, and will have to borrow less for college.

As the father of a young child, my wife and I have to think carefully about every financial choice we make. For example, right now we're trying to decide what to do with our slightly bigger than usual tax refund. I imagine that there are many other young families in the same situation as us right now—about to receive the biggest sum of discretionary money we'll likely see all year, and no shortage of important things to spend it on.

Part of MEFA's mission, and something that I have done personally in my job here, is to try to convince parents how important it is to save for college and to start as early as possible. One of the savings strategies that we recommend is to use some of your tax refund to start or contribute to your child's college savings fund.

So now here I am with a chance to put my money where my mouth is. And to my chagrin, it's a little harder than I imagined. The thought of paying off a credit card balance, or getting that new furniture for the bedroom, or going on vacation is admittedly more tempting than saving for college. But here's why I'm still going to do it:

- I've talked to many people who have saved for college and many who haven't. Those who have saved are generally better equipped to navigate the financial aid waters when the time comes, in part because they are much less anxious. Thinking through college costs is not completely new to them, and they have done some preparation. No one has ever regretted saving for college.

- I know I can't save the whole cost of college, but I probably don't have to. Because of the amount of financial aid available, you are not likely to pay the entire cost of college yourself. And since the financial aid formula counts a family's income more than their savings, I know that saving early and often for my son won't affect financial aid very much. A little savings can help a lot.

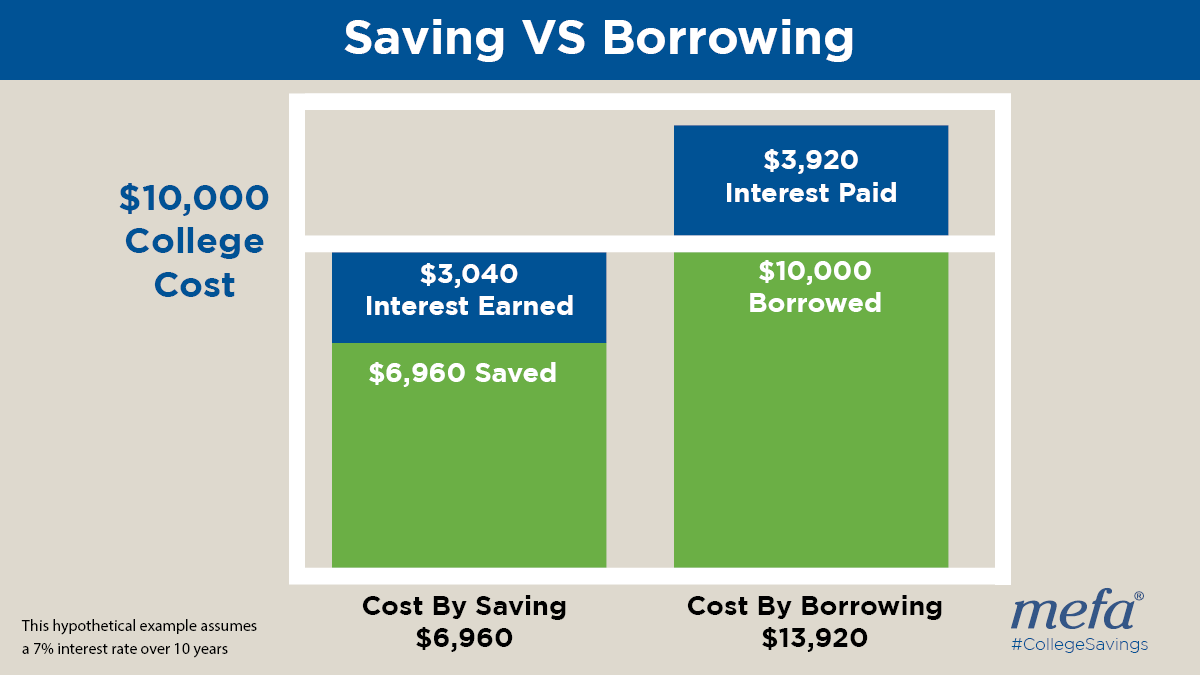

- I don't want to borrow everything. Many students and families find themselves in the position of graduating from school and having to pay a student loan bill every month that is just too much for them to afford. This is obviously a bad spot to be in and I'm going to take steps now to help avoid that. The graphic below shows that financing a $10,000 college cost looks very differently for a family that has saved versus a family needing to borrow the entire sum. Remember, earning interest is better than paying interest.

- If your child knows that you are putting money away to pay for his or her college costs, he or she will be more likely to attend school. According to a study from the University of Kansas, low-income students who have any college savings are 3 times more likely to attend college than those who don't, and they are 4 times more likely to graduate.

Even with the knowledge that I have, and after all of this advice, I still know how it feels, and it's not easy. There are so many other things that need to be done right now, and with college so far away, saving for it is a distant worry. But time will take care of the distance. What we do about the worry is up to us.

Sign Up for Emails

Sign up for relevant, helpful college planning emails.